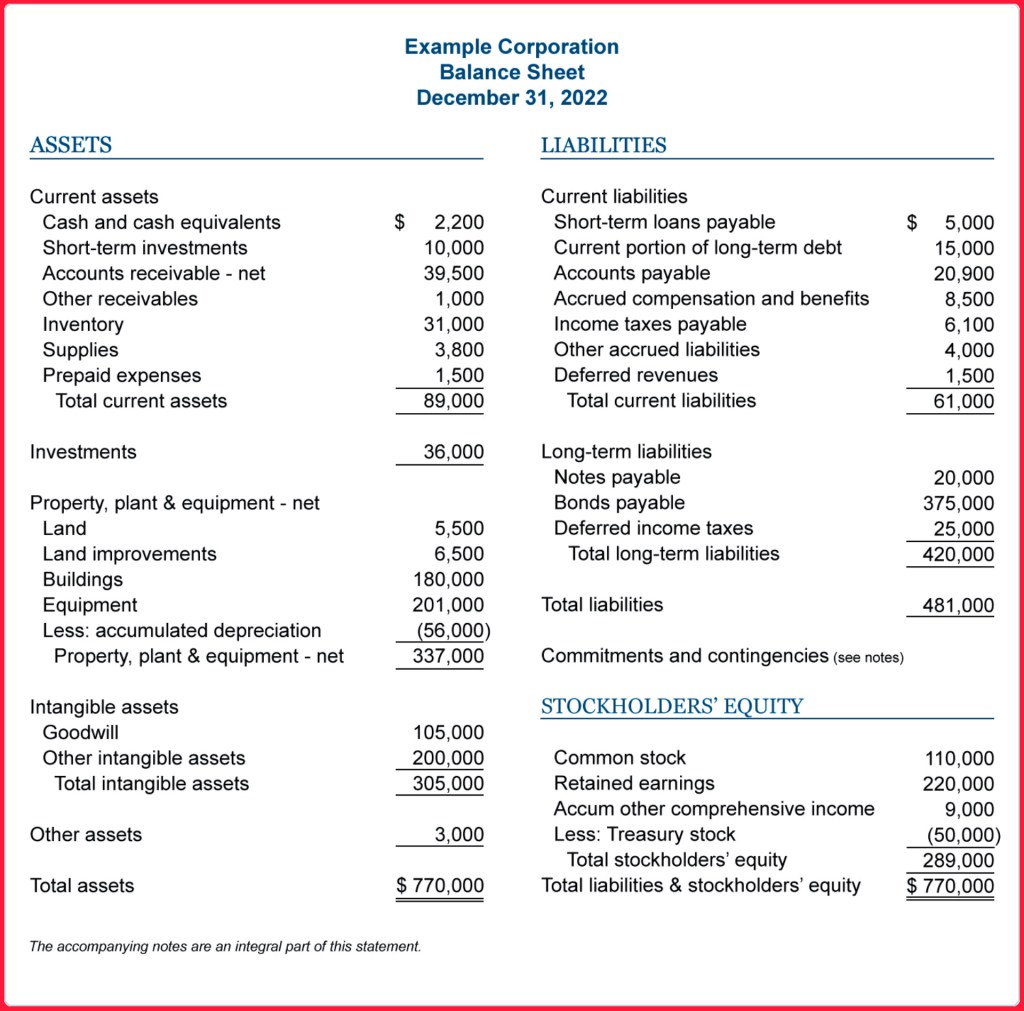

A balance sheet is a financial statement that provides a snapshot of a company’s financial position at a specific point in time. The balance sheet presents the assets, liabilities, and equity of the company and shows how these three components are related to each other. Here is a detailed explanation of each component of a balance sheet:

Assets:

Assets are the resources that a company owns or controls and are expected to provide future economic benefits. They are classified into current assets and non-current assets.

a. Current assets:

These are assets that can be easily converted into cash within a year or a normal operating cycle of the business. Examples of current assets include cash and cash equivalents, accounts receivable, inventory, and prepaid expenses.

b. Non-current assets:

These are assets that are expected to provide economic benefits for more than one year. Examples of non-current assets include property, plant and equipment (PP&E), intangible assets, and long-term investments.

Liabilities:

Liabilities are the obligations that a company owes to others, including suppliers, employees, and lenders. They are classified into current liabilities and non-current liabilities.

a. Current liabilities:

These are liabilities that are due within a year or a normal operating cycle of the business. Examples of current liabilities include accounts payable, accrued expenses, and short-term debt.

b. Non-current liabilities:

These are liabilities that are due after one year. Examples of non-current liabilities include long-term debt, deferred tax liabilities, and pension liabilities.

Equity:

Equity represents the residual interest in the assets of the company after deducting the liabilities. Equity includes the capital contributed by the owners and the retained earnings of the company.

a. Capital contributed by owners:

This includes the amount of money that the owners have invested in the company in exchange for ownership. Examples of capital contributed by owners include common stock and preferred stock.

b. Retained earnings:

This represents the accumulated profits of the company that have not been distributed to the owners as dividends.

In summary, the balance sheet shows the company’s assets on the left-hand side and its liabilities and equity on the right-hand side. The total assets must always equal the total liabilities and equity, as the balance sheet follows the accounting equation: Assets = Liabilities + Equity.

Leave a comment